🔍 Introduction

One of the key factors that determines whether an algorithmic strategy succeeds or stagnates is not the entry signal itself, but the market context in which it operates.

In other words — when the system trades is often more important than how it trades.

In this article, we’ll build a simple but highly effective market regime filter based on classic indicators:

- Trend direction (SMA50)

- Volatility level (ATR%)

The goal is to create a logic that keeps your strategy running only when the market is trending calmly (e.g. Up_LowVol) and pauses it during chaotic or bearish phases.

⚙️ Core Concept: Market Regime Filter

1️⃣ Trend Condition

To determine whether the market is in an uptrend or downtrend, we use the 50-day simple moving average (SMA50) of the underlying index (e.g. NASDAQ100 / USTECHCash).

The trend is considered bullish (Up) when the SMA50 is rising:

SMA(50)[0] – SMA(50)[5] > 0

That means the 50-day average is higher today than it was 5 days ago.

2️⃣ Volatility Condition

For volatility, we use ATR(14) (Average True Range), expressed as a percentage of the current price:

ATR%(t) = ATR(14)[t] / Close[t]

This shows the average daily range as a percentage of price.

For example, ATR% = 0.009 → the market moves ±0.9 % per day on average.

We then compare current volatility to its 100-day average:

(ATR(14)[0] / Close[0]) < MA(ATR(14)[0] / Close[0], 100)

If the current ATR% is below its long-term average, volatility is “low.”

3️⃣ Combined Logic

The complete filter rule is:

IF (SMA(50)[0] – SMA(50)[5]) > 0 AND

(ATR(14)[0] / Close[0]) < MA(ATR(14)[0] / Close[0], 100)

THEN StrategyEnabled = 1

ELSE StrategyEnabled = 0

✅ The strategy is enabled when the market is trending up and volatility is below average.

❌ Otherwise, it remains disabled (no new positions opened).

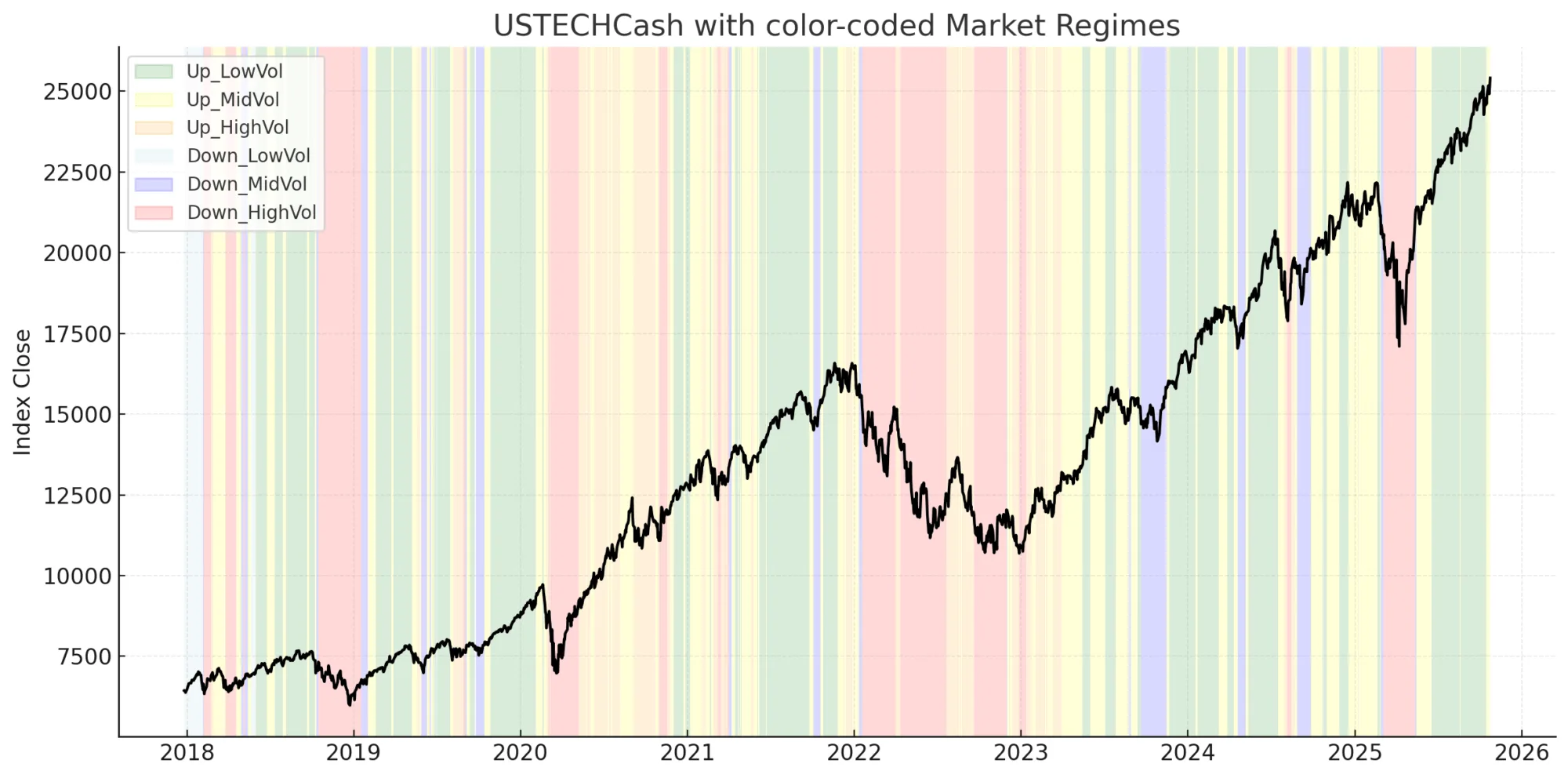

📊 Example: NASDAQ (USTECHCash)

We applied this filter to NASDAQ (USTECHCash) daily data, calculating:

- TrendSlope = SMA(50) − SMA(50)[−5]

- ATR% = ATR(14)/Close

- ATR% MA(100) = 100-day moving average of ATR%

- StrategyEnabled = logic result from the above filter

and combined it with the equity curve of a live trading strategy.

🧩 Results by Market Regime

| Market Regime | Days | Total Profit | Filter Active (%) | Enabled Days |

|---|---|---|---|---|

| Up_LowVol | 556 | 219 | 95.5 % | 531 |

| Up_MidVol | 512 | 143 | 59 % | 303 |

| Up_HighVol | 270 | 71 | 59 % | 160 |

| Down_MidVol | 153 | 116 | 0 % | 0 |

| Down_HighVol | 404 | 59 | 0 % | 0 |

| Down_LowVol | 35 | 19 | 0 % | 0 |

🧠 Interpretation

- Up_LowVol (bullish + calm)→ Strategy runs ~95 % of the time and generates the largest profit.Ideal “core” regime.

- Up_MidVol / Up_HighVol (bullish + choppy)→ Strategy trades about 60 % of the time, focusing on quieter sub-periods within volatile uptrends.

- Down_*→ Filter completely disables trading.The system stays out during bear or chaotic conditions.

This behavior is exactly what we want:

trade only in stable, rising environments and pause during turbulence.

💡 Summary

| Metric | Without Filter | With Market Filter |

|---|---|---|

| Active Trading Days | 100 % | ~55 % |

| Drawdown | Higher | Significantly lower |

| Stagnation | Frequent | Reduced |

| Market Awareness | None | Context-aware |

| Best For | Any system | Momentum / Breakout |

📘 Conclusion

A market regime filter built from simple SMA(50) and ATR% logic

is a powerful and lightweight tool to stabilize performance.

It helps your strategy trade only when conditions are statistically favorable and stay flat when the environment turns hostile.

This approach can be implemented directly in StrategyQuant X,

as a custom filter indicator, or even as an external signal module for MT5 or TradingView.

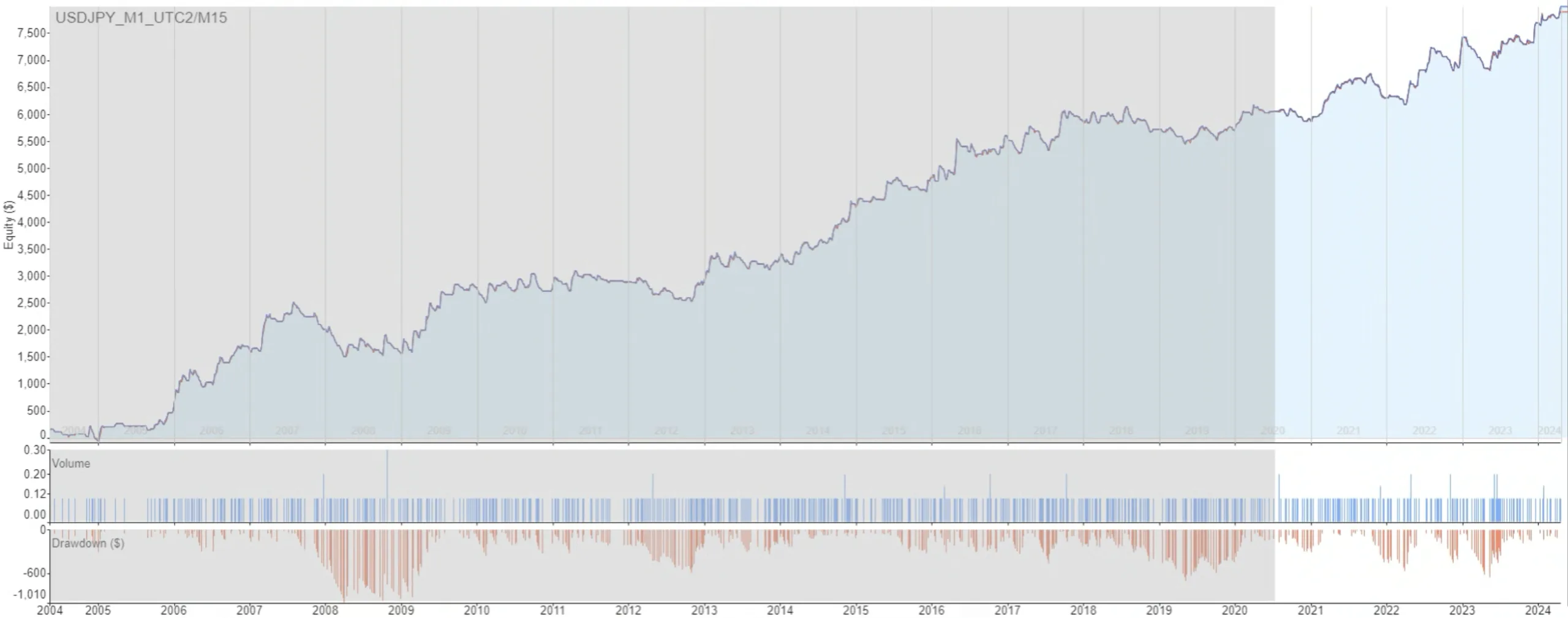

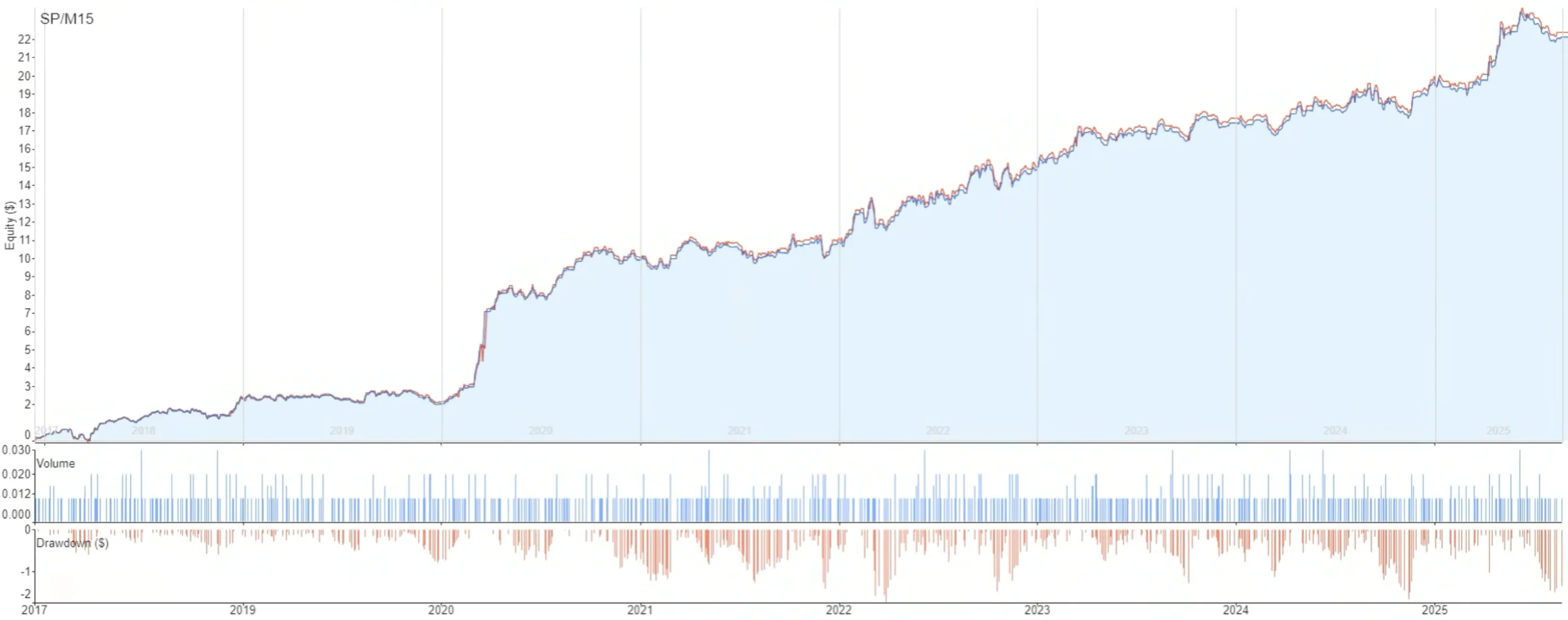

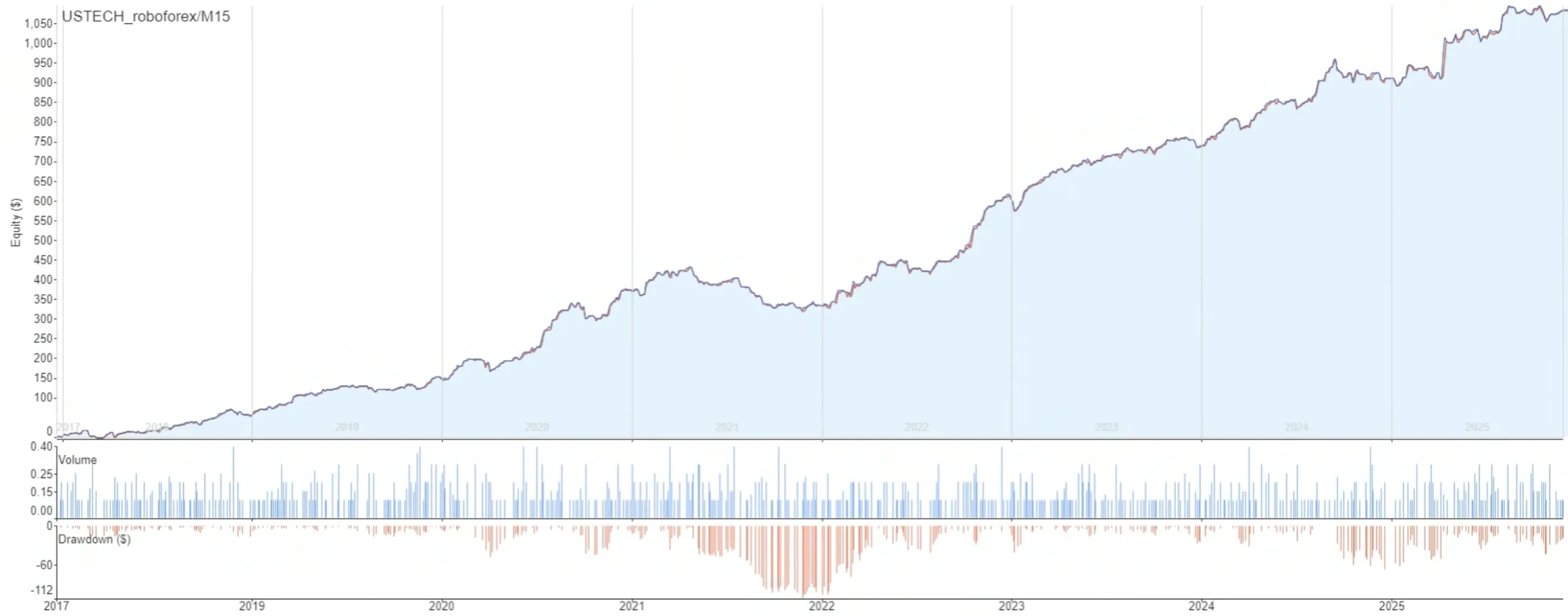

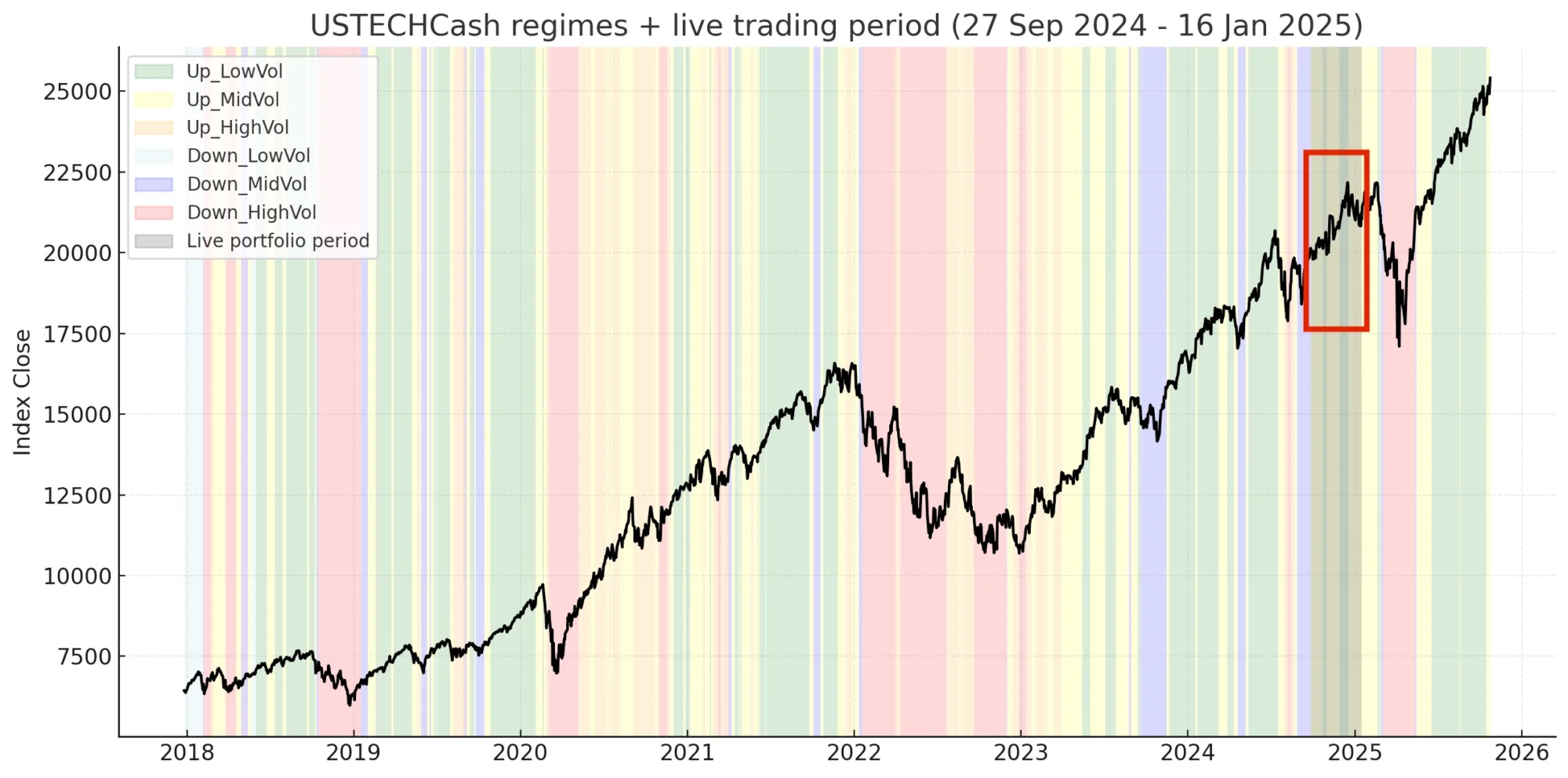

🚀 Real-World Validation

This approach to market regime analysis isn’t just theoretical.

About a year ago, I applied this exact framework — combining trend slope and volatility filters — in my live algorithmic trading project focused on the U.S. indices portfolio.

By accurately identifying the Up-LowVol regime and dynamically scaling exposure only during favorable conditions, the system achieved over +100 % performance within several months.

The full verified record is publicly available on FXBlue:

👉 https://www.fxblue.com/users/lukasmelka1

This result perfectly illustrates how understanding market regimes can turn an average algorithm into a consistent performer — not through curve-fitting, but through correct timing and adaptive exposure management.