Correct Builder Settings in SQ: Why Fixed SL, TP and Trailing Stops Must Be Normalized Per Market

When building strategies across multiple instruments, one of the most common hidden mistakes is using the same fixed-point stop loss, take profit or trailing stop range for every symbol. The number may look identical in the Builder, but the real market meaning can be completely different.

The Core Problem

A fixed stop loss of 35 points may look like a simple technical setting. However, 35 points on Brent, Gold, Dow, BTCUSD or EURJPY does not represent the same price movement.

This is especially dangerous when the strategy uses fixed stop loss, fixed take profit or fixed trailing stop values. If those values are not adjusted per symbol, one market may receive a realistic exit distance, while another market may receive an exit that is so tight that trades are closed almost immediately.

The Simple Normalization Formula

Before setting fixed-point ranges in SQ Builder, we should convert price movement into points and compare it across markets.

The point size must always be verified from the broker or MT5 symbol specification. In this comparison, the point size was inferred from the actual stop loss distance in the exported trades.

How Much Is a 35-Point Stop Loss on Each Market?

The table below shows why a fixed 35-point stop loss cannot be reused blindly across instruments.

| Market | Average Open Price | Inferred Point Size | 35 Points Price Move | 35 Points as % of Price | Points for 1% Move |

|---|---|---|---|---|---|

| BRENT | 74.49 | 0.01 | 0.35 | 0.470% | 74 |

| BTCUSD | 79,394.04 | 0.01 | 0.35 | 0.00044% | 79,394 |

| DOW | 48,589.22 | 0.10 | 3.50 | 0.0072% | 4,859 |

| EURJPY | 184.39 | 0.01 | 0.35 | 0.190% | 184 |

| XAUUSD | 4,753.37 | 0.01 | 0.35 | 0.0074% | 4,753 |

Strategy Result Comparison

The tested strategy used a fixed 35-point stop loss. The same exit scale behaved very differently across markets.

| Market | Trades | Net P/L | Profit Factor | Win Rate | Exit Structure |

|---|---|---|---|---|---|

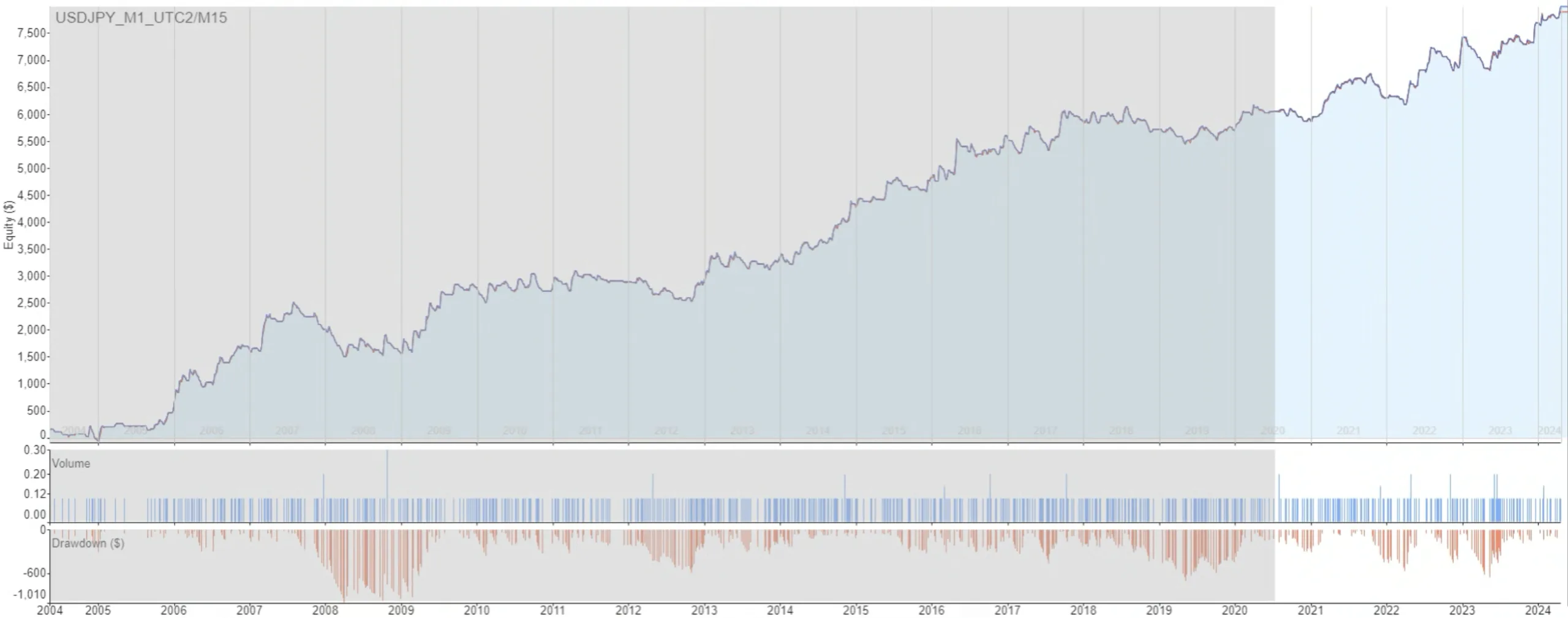

| BRENT | 16 | +46.48 | 2.10 | 25.0% | 12× SL, 1× PT, 2× Exit after bars, 1× Friday exit |

| BTCUSD | 17 | 0.00 | n/a | 0.0% | 17× SL |

| DOW | 17 | -0.68 | 0.00 | 0.0% | 17× SL |

| EURJPY | 11 | +9.84 | 1.86 | 54.5% | 5× SL, 1× PT, 4× Exit after bars, 1× Friday exit |

| XAUUSD | 8 | -2.80 | 0.00 | 0.0% | 8× SL |

The conclusion is not simply that the strategy works on Brent and EURJPY and fails on BTCUSD, DOW and XAUUSD. The more important conclusion is that the exit scale is not comparable.

Recommended SQ Builder Ranges by Percentage Move

A better workflow is to define the intended market movement first and then convert it into Builder points for each symbol.

| Market | 0.2% Move | 0.5% Move | 1.0% Move | 2.0% Move |

|---|---|---|---|---|

| BRENT | 15 | 37 | 74 | 149 |

| BTCUSD | 15,879 | 39,697 | 79,394 | 158,788 |

| DOW | 972 | 2,429 | 4,859 | 9,718 |

| EURJPY | 37 | 92 | 184 | 369 |

| XAUUSD | 951 | 2,377 | 4,753 | 9,507 |

Why Universal Fixed-Point Ranges Are Dangerous

A universal range such as 10–200 points may look convenient, but it has a completely different meaning across markets.

- On Brent, 10–200 points can represent a meaningful intraday range.

- On EURJPY, the same range can still be usable.

- On Gold or Dow, the range may be far too tight.

- On BTCUSD, even thousands of points may still represent a relatively small percentage move.

This means that a cross-market Builder configuration must not be copied mechanically. The same numerical setting can create completely different behavior.

Correct Workflow for SQ Builder

Before building strategies with fixed-point exits, the Builder setup should follow a normalized process.

| Step | What to Do | Why It Matters |

|---|---|---|

| 1 | Check the current market price. | The same point distance has a different percentage meaning on each instrument. |

| 2 | Check the symbol point size. | Broker specifications can differ between symbols and accounts. |

| 3 | Define the intended movement in percent or ATR. | This describes the real market behavior you want the strategy to capture. |

| 4 | Convert that movement into Builder points. | This creates a realistic parameter range for the selected market. |

| 5 | Build each market with its own fixed-point range. | This makes the strategy generation process comparable and fair. |

ATR-Based and Percent-Based Exits Are Often Safer

Fixed-point exits are not wrong. The problem is that they require careful normalization.

ATR-based exits automatically adapt to current volatility. Percent-based exits automatically adapt to the price level of the instrument. Fixed-point exits only work safely when their scale is adjusted manually for each symbol.

Conclusion

Correct Builder settings in StrategyQuant X are not only about choosing entry conditions, filters and robustness tests. The scale of SL, TP and trailing stop parameters is just as important.

If fixed-point exits are used, each instrument needs its own normalized range. Without this step, the Builder may generate or reject strategies for the wrong reason.

A strategy may not be failing because the entry logic is weak. It may simply be failing because the stop loss, take profit or trailing stop range is mathematically incompatible with the market.

The correct workflow is simple: define the intended movement in percent or ATR terms, convert it into Builder points for each symbol, and only then compare strategy performance across markets.