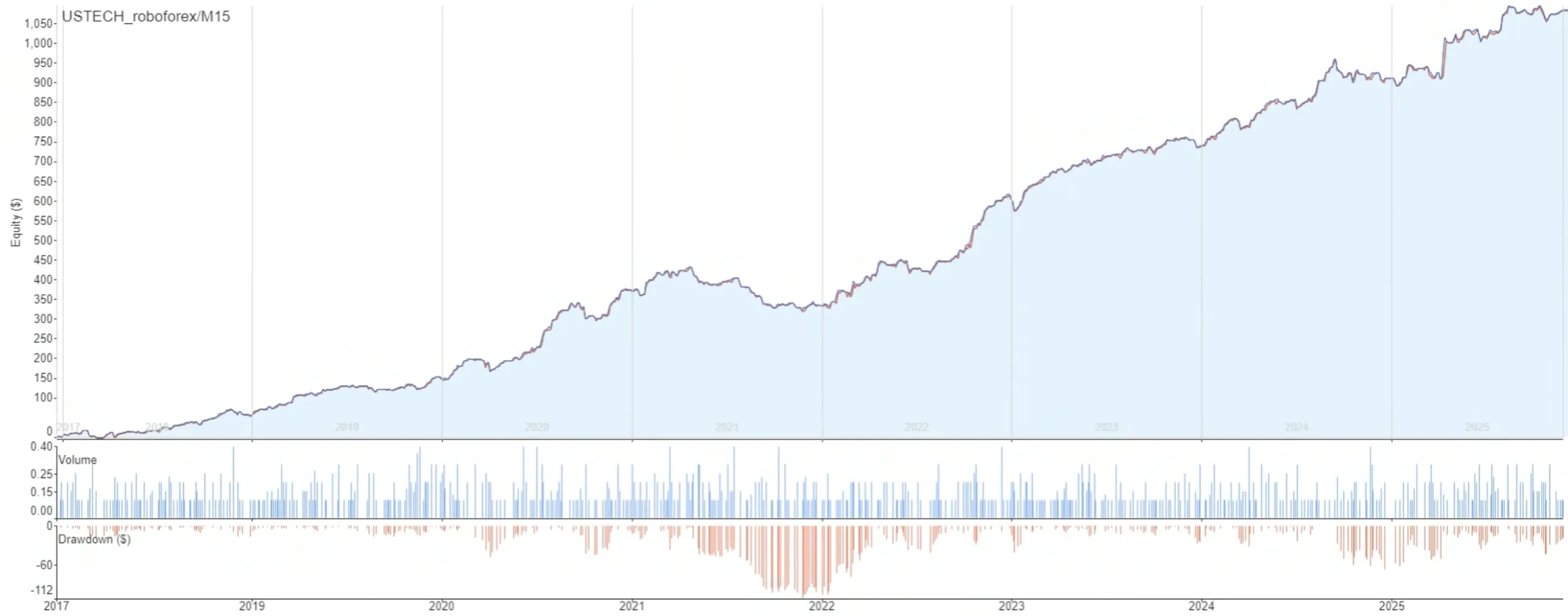

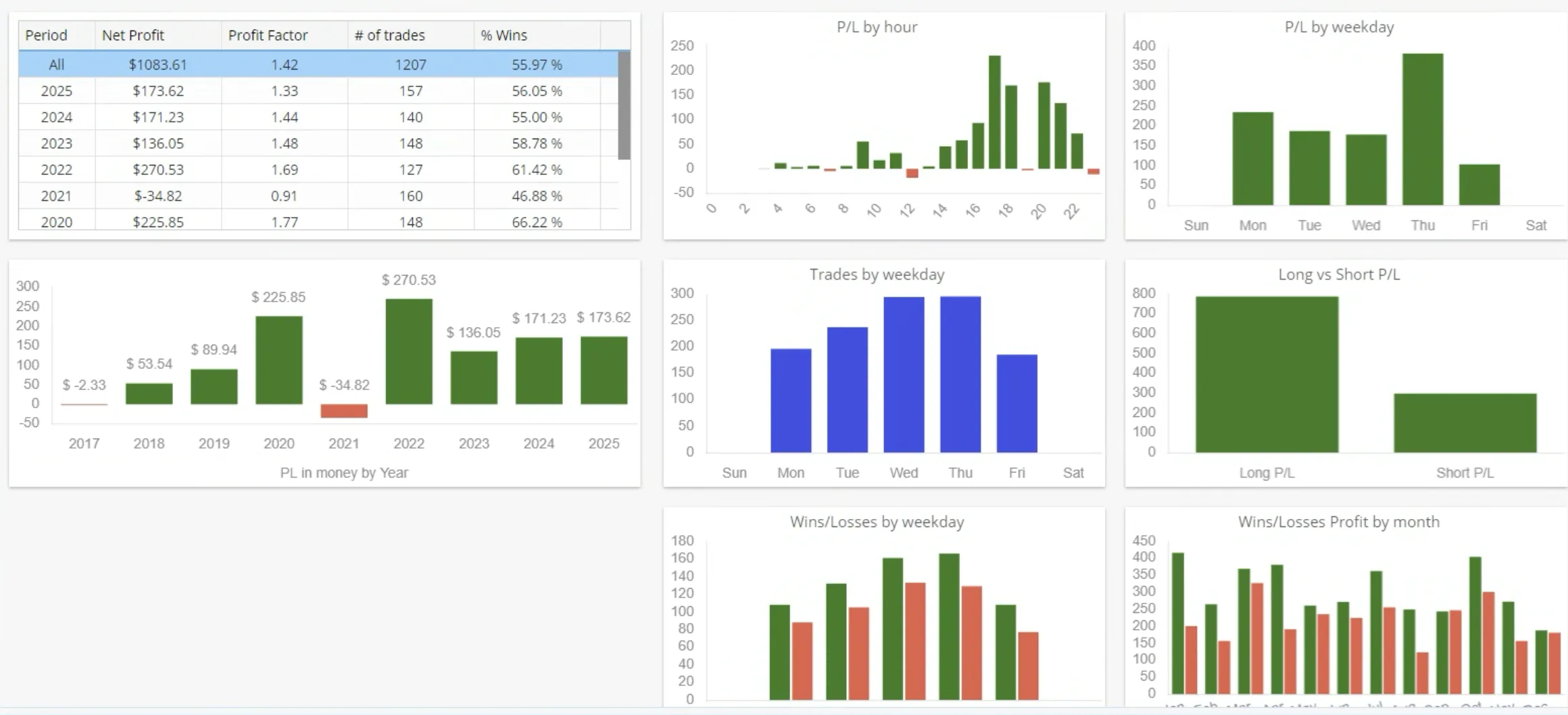

Profit factor 1.42

Instrument: Index

Supported platforms: MetaTrader 4, MetaTrader 5, StrategyQuant

Strategy description

The NQ Keltner Pulse M15 Strategy is a structured rule-based breakout system designed for the Nasdaq / NQ M15 market. Its goal is to participate when the market confirms a strong directional impulse outside its normal Keltner Channel structure, while using volatility-adjusted pending STOP orders for more disciplined execution.

The strategy uses the Keltner Channel as its primary market structure filter. A long setup is created when price closes above the upper Keltner Channel, showing bullish momentum and possible continuation pressure. A short setup is created when price closes below the lower Keltner Channel, showing bearish momentum and possible downside continuation.

Once the directional condition is confirmed, the system does not enter immediately at market. Instead, it places a pending STOP order around the recent daily reference level, adjusted by an ATR-based volatility buffer. This allows the strategy to wait for additional price confirmation before entering the trade.

For long setups, the strategy places a Buy Stop around the daily high reference level, shifted by 0.1 × ATR. For short setups, it places a Sell Stop around the daily low reference level, shifted by the same ATR-based buffer. Pending orders remain valid for 46 bars, duplicate trades are disabled, and pending order replacement is enabled.

Risk management is volatility-adjusted. Each trade uses a stop-loss based on 2.5 × ATR and a profit target set at 1.5 percent from the entry price. In addition, the strategy uses a trailing stop of 100 points, activated after the trade moves approximately 1.8 × ATR in the favorable direction.

The system also applies a time-based exit after 30 bars and closes open trades on Friday at 19:00 to reduce weekend exposure.

Market: Nasdaq / NQ

Timeframe: M15

Entry logic: Keltner Channel breakout + ATR-adjusted pending STOP entry

Market structure filter: Keltner Channel

Volatility filter: ATR buffer

Order type: Pending STOP orders

Keltner Channel period: 20

Keltner Channel multiplier: 2.6

Entry buffer: 0.1 × ATR

Stop-loss: 2.5 × ATR

Profit target: 1.5 %

Trailing stop: 100 points

Trailing activation: 1.8 × ATR

Time exit: 30 bars

Pending order expiration: 46 bars

Duplicate trades: Disabled

Pending order replacement: Enabled

Friday exit: 19:00

Overall, this strategy is built for traders who prefer a systematic momentum breakout framework combining Keltner Channel market structure, ATR-adjusted pending entries, volatility-based risk management, trailing protection, and disciplined execution on the Nasdaq market.