How Collective Behavior Creates Order in Markets

Introduction: Markets Are Not Individual Systems

Markets are often described as mechanisms driven by rational decisions. This description fails at the most basic level.

Markets do not act.

Individuals do.

But markets move.

The difference lies in aggregation. When individual decisions interact under uncertainty, collective behavior emerges. This behavior is not random. It follows recognizable patterns that repeat across time, instruments, and generations.

Market structure is not imposed externally.

It is produced internally by the crowd.

Markets as Social Systems

Every market transaction is a social act.

It reflects:

- expectation

- imitation

- fear of exclusion

- desire for confirmation

No participant acts in isolation. Each decision is influenced by observation of others, even when that influence is indirect. Price itself becomes a communication channel through which the crowd signals belief, doubt, and conviction.

Structure emerges not because participants agree, but because their reactions align under pressure.

Why Crowds Behave Predictably Under Uncertainty

Uncertainty compresses decision-making.

When outcomes are unclear, individuals seek reference points. They look to price behavior, recent outcomes, and visible participation. As uncertainty rises, imitation increases.

This is not irrational behavior. It is adaptive.

Crowds behave predictably not because individuals are foolish, but because information arrives unevenly and interpretation lags reality. By the time consensus forms, structure has already developed.

From Individual Emotion to Collective Structure

Individual emotions cancel each other out.

Fear in one participant is offset by confidence in another. Optimism meets skepticism. At the individual level, behavior is noisy.

At the collective level, it is directional.

Structure emerges only after aggregation. Trends, ranges, and extremes are not expressions of individual belief, but of collective alignment over time.

This is why market structure cannot be explained psychologically at the individual level. It exists only at scale.

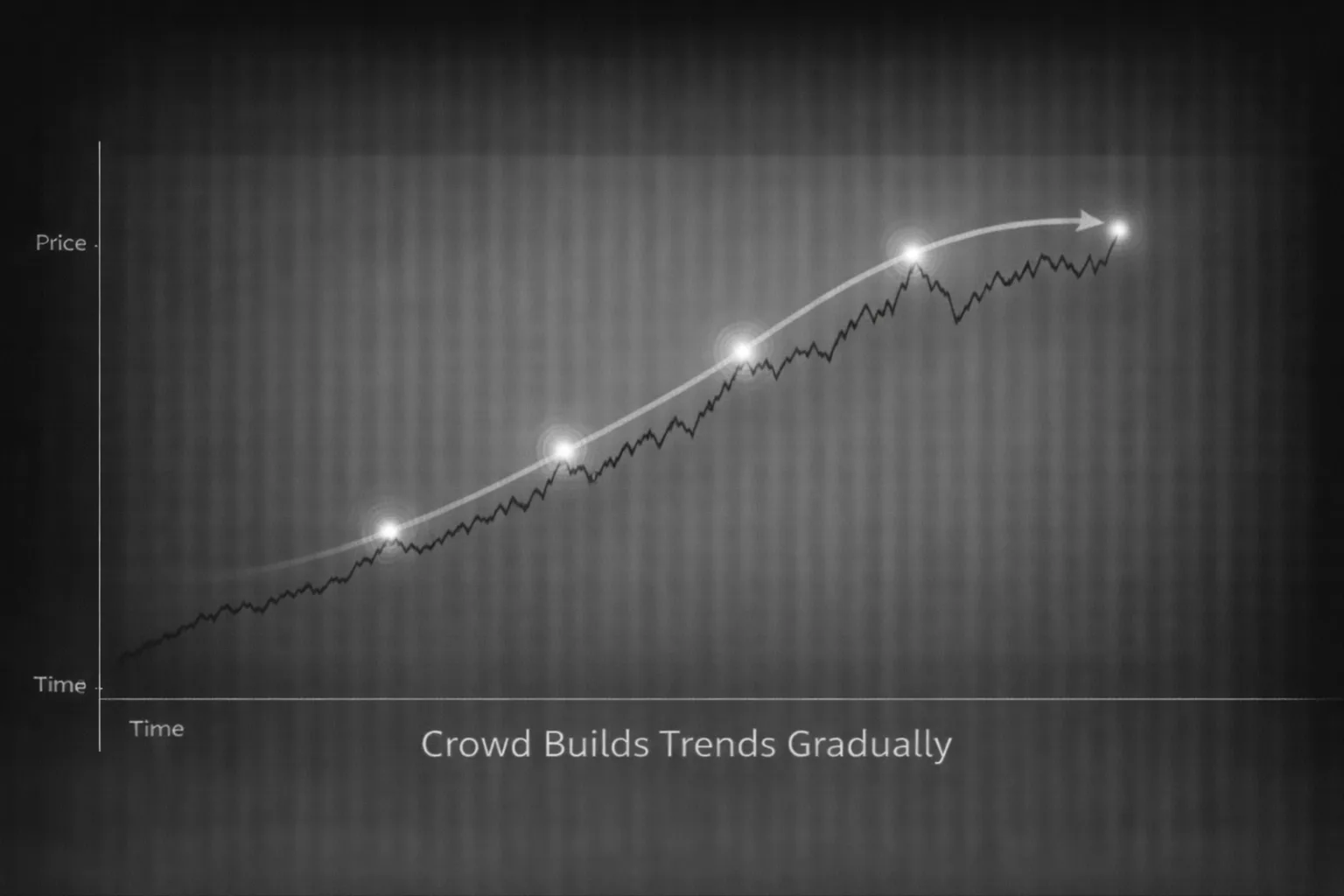

Crowd Psychology and Trend Formation

Trends do not begin with consensus.

They begin with imbalance.

Early participants act with limited confirmation. As price persists, observation turns into participation. The crowd does not move at once — it joins progressively.

This delayed participation is what sustains trends. The more visible a trend becomes, the more capital remains uncommitted, waiting for confirmation. Ironically, widespread recognition arrives near structural maturity.

Trends strengthen not because everyone agrees, but because not everyone has acted yet.

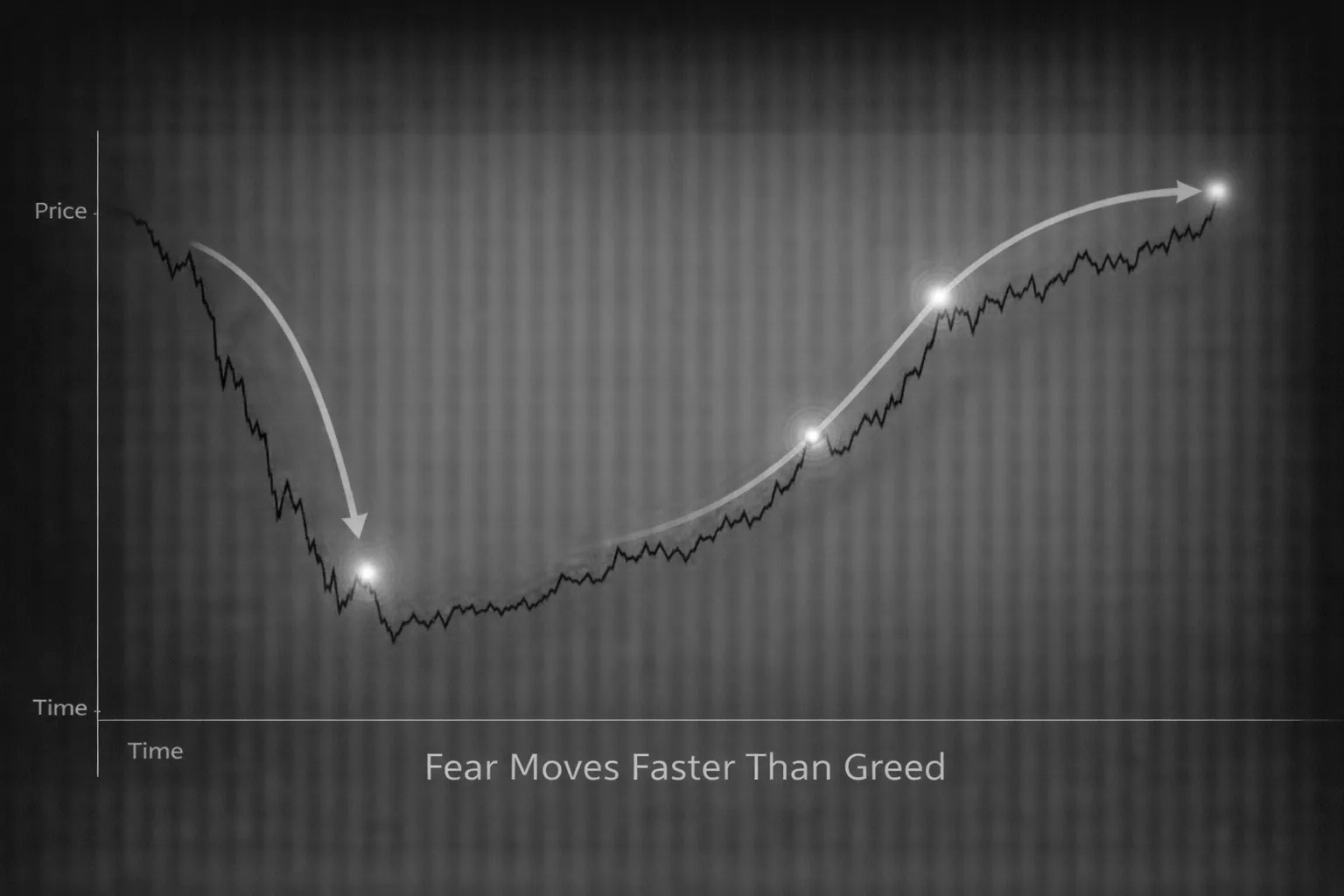

Fear, Greed, and Structural Asymmetry

Fear and greed are not symmetric forces.

Fear is:

- rapid

- synchronized

- self-reinforcing

Greed is:

- gradual

- fragmented

- delayed

This asymmetry explains why declines accelerate faster than advances, and why bottoms form abruptly while tops distribute slowly. Crowd psychology introduces directional bias into market structure.

Structure reflects this imbalance. It is not emotional chaos — it is patterned behavior.

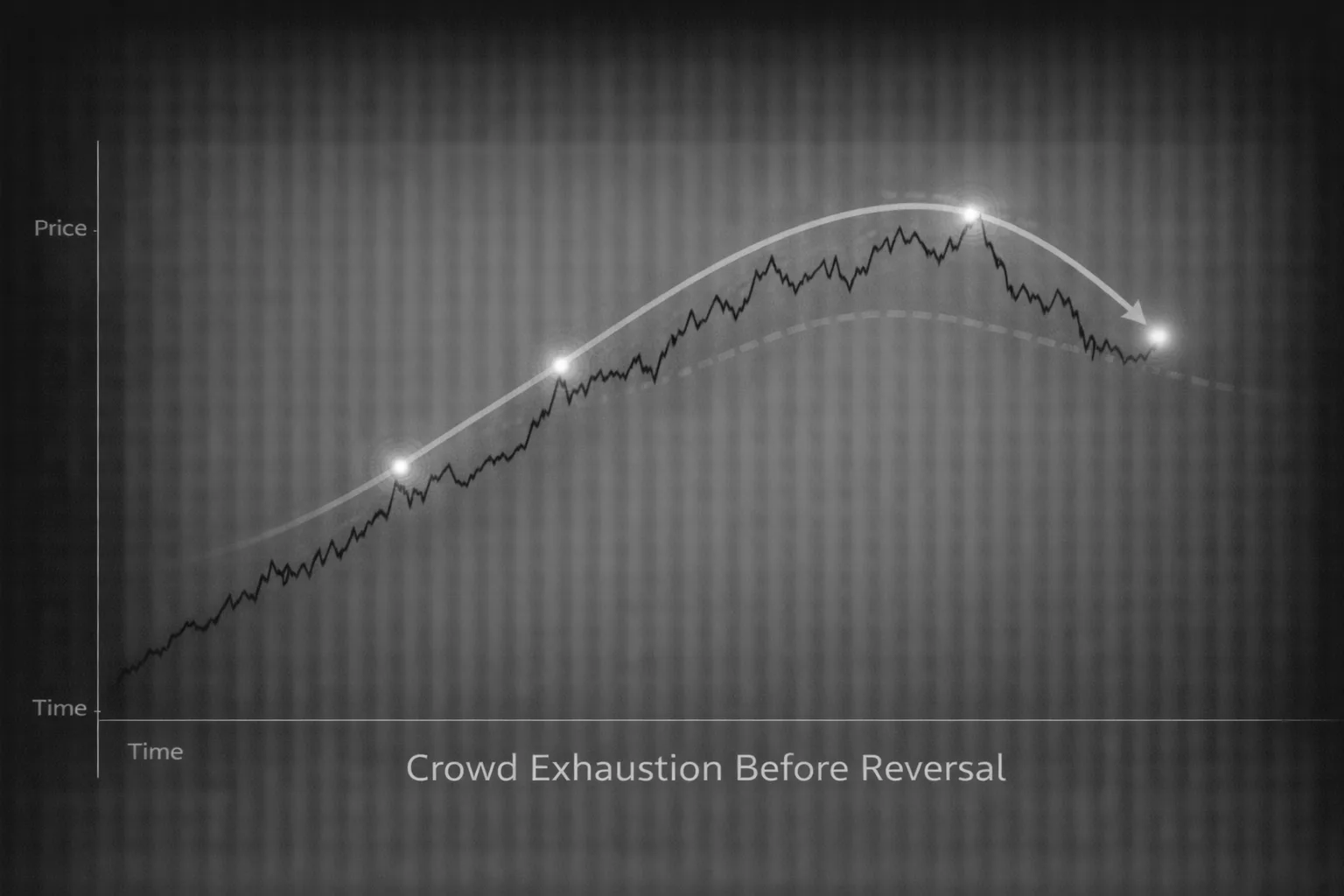

Crowd Exhaustion and Structural Breakdown

Crowd participation is finite.

Trends persist only while new participants continue to enter. When that flow slows, structure begins to degrade. Price does not collapse immediately. It loses momentum.

This phase is often misunderstood. Exhaustion is not reversal. It is loss of reinforcement.

Markets stall not because belief disappears, but because additional belief cannot be mobilized.

Structure weakens before direction changes.

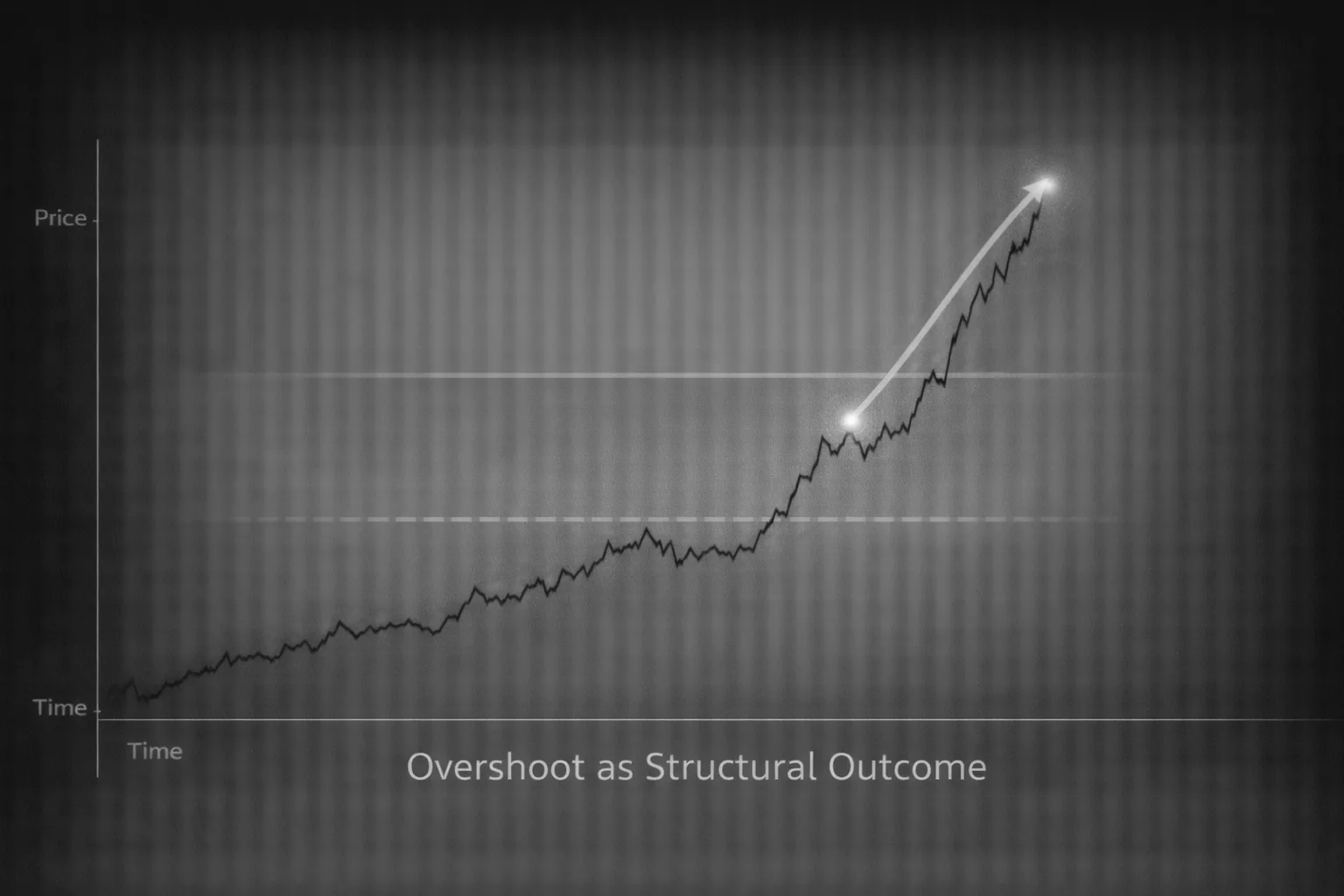

Why Markets Overshoot

Markets overshoot because crowds do not stop at equilibrium.

Once participation aligns, feedback loops develop. Rising prices validate belief. Validation attracts participation. Participation reinforces structure.

Overshoot is not error.

It is the natural outcome of collective reinforcement.

Fair value is irrelevant in crowd-driven environments. Structure continues until participation saturates or breaks.

Public Perception Versus Structural Reality

Crowds narrate markets in hindsight.

Phases are named only after they end. “Bull market” and “bear market” are retrospective labels, not operational states. During transitions, perception lags structure.

This gap between perception and reality is where volatility expands. Media narratives chase outcomes. Structure evolves independently.

Understanding markets requires separating what the crowd says from what the crowd does.

Crowd Psychology Across Timeframes

Crowd behavior scales.

Intraday traders form micro-crowds. Swing traders form intermediate collectives. Long-term investors form macro crowds. The structure is identical — only the timeframe differs.

Persistence, exhaustion, overshoot, and breakdown appear at every scale. Time compresses or expands the pattern, but does not change it.

Structure is fractal because behavior is.

Implications for Systematic Traders

Systems fail when they ignore crowd context.

Mechanical rules assume stability. Crowds introduce instability. When participation clusters, volatility shifts and correlations rise. Strategies designed for equilibrium environments degrade under crowd pressure.

Crowd psychology is not a signal.

It is environmental context.

Robust systems adapt their expectations to crowd state rather than attempting to predict outcomes.

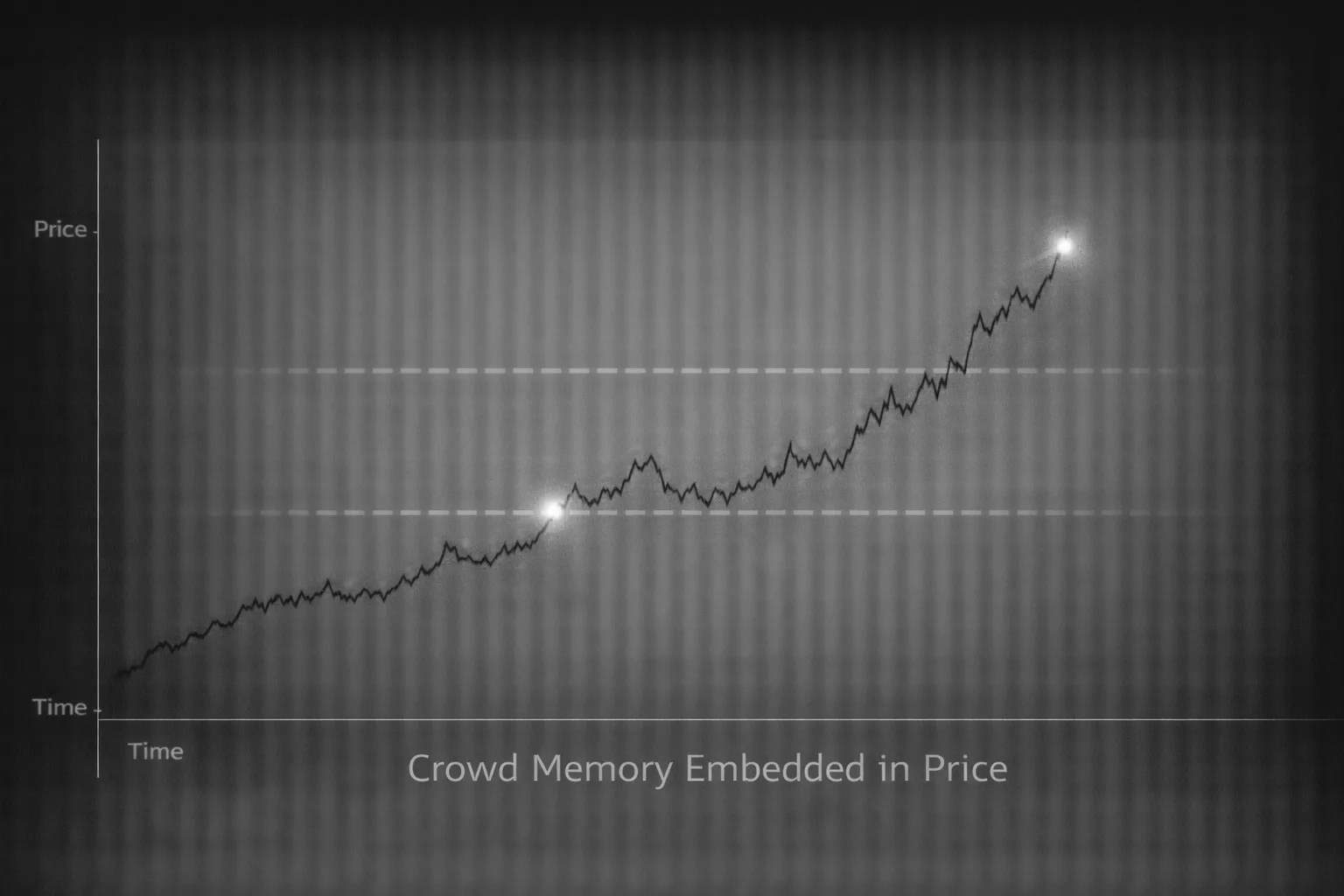

Conclusion: Market Structure Is Crowd Memory

Markets remember.

Not consciously, but structurally. Past crowd behavior leaves imprints that shape future movement. Support, resistance, trends, and ranges are memory traces of collective experience.

Crowd psychology does not disrupt structure.

It creates it.

Markets are not random because crowds are not random. They are adaptive, imitative, and constrained by time. Structure is the visible residue of that process.

Understanding markets, therefore, requires understanding crowds — not as emotions, but as systems of behavior under uncertainty.