A new market is only worth adding if it does something the markets you already trade don't — and if it survives realistic costs once you stop flattering it. RoboForex now lists BTCUSD, so I downloaded the M1 history, started building algorithmic strategies on it, and ran a first five-market portfolio preview. This is the research so far — numbers included, trade-offs and all.

My live portfolio isn't a pile of correlated systems. It's four structurally different markets — XAUUSD, .US30Cash, BRENT and EURJPY — chosen so each pulls its weight in conditions where the others stall. The question I'm testing now is simple: can a crypto market earn a fifth seat?

Why test BTCUSD at all

The point of a portfolio isn't more strategies — it's different strategies. Highly correlated systems just stack the same risk under different names. RoboForex now lists BTCUSD in its contract specifications, which opens the door to a genuinely different source of return: a market driven by its own cycle, largely uncoupled from gold, indices and FX.

So I pulled M1 history for BTCUSD and started generating builds. The goal at this stage is research and validation, not a launch: find robust logic, test it across conditions, and check whether it still means anything inside a broader portfolio.

The strongest direction so far

The best results in this phase come from our Premium Fibonacci template, running on the H4 timeframe. (It's one of the templates included with Premium membership.) That's where the most testing and validation effort is now going — one clear direction, tested hard, rather than a spread of half-checked ideas.

Preparing the data honestly

Crypto data needs more care than a major FX pair, and this is where most BTCUSD backtests quietly lie to their authors. In the RoboForex tick history I used, I found two problems:

- a gap with missing data, which distorts the market behaviour the builder actually sees, and

- historical spread conditions that needed adjustment before they could drive realistic builds.

So I normalised the spread before running the generator. Not to make the results prettier — the opposite. Distorted spread values manufacture entries and exits that never could have filled, and produce strategies that look attractive only because the costs were wrong. Missing data and unrealistic spreads are how a curve-fit gets mistaken for an edge. On crypto, execution and cost validation have to be stricter, not looser.

The five-market portfolio preview

To see the portfolio effect, I combined BTCUSD with the four existing markets. The calculation starts from zero equity and uses closed backtest trades only, including profit, swap and commissions.

| Metric | Value |

|---|---|

| Markets | 5 (including BTCUSD) |

| Closed trades | 2,454 |

| Net result | +5,135.40 |

| Profit factor | 1.63 |

| Max drawdown | −158.71 |

| Profitable months | 79 / 101 (78.22%) |

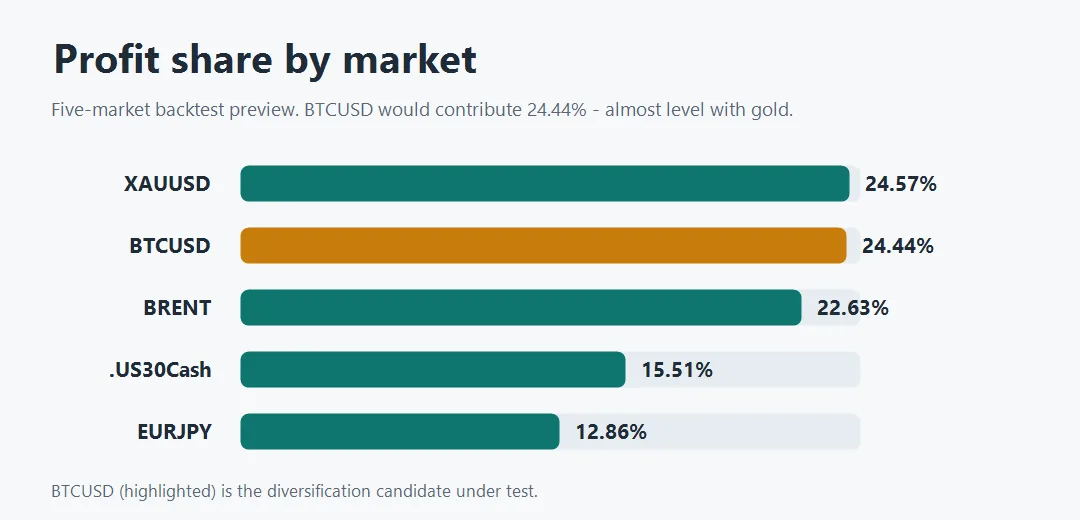

Broken down by market:

| Market | Trades | Net result | Profit factor | Win rate | Max DD | Profit share |

|---|---|---|---|---|---|---|

| XAUUSD | 473 | +1,261.89 | 1.96 | 54.76% | −90.90 | 24.57% |

| BTCUSD | 708 | +1,254.93 | 1.44 | 32.49% | −131.21 | 24.44% |

| BRENT | 326 | +1,162.12 | 1.74 | 34.66% | −73.94 | 22.63% |

| .US30Cash | 511 | +796.29 | 1.70 | 44.23% | −66.38 | 15.51% |

| EURJPY | 436 | +660.17 | 1.51 | 47.94% | −86.30 | 12.86% |

| Portfolio total | 2,454 | +5,135.40 | 1.63 | 42.26% | −158.71 | 100.00% |

All figures are relative backtest units, from zero equity, after profit, swap and commission. Past performance does not guarantee future results.

Positive in every tested year

The five-market preview finished positive in every calendar year tested. The strongest completed year was 2025 (+1,035.54); the 2026 figure reflects only the partial period in the database, up to 21 May 2026.

What BTCUSD actually adds — and what it costs

Here's where you have to resist the profit number. In this preview BTCUSD contributes +1,254.93 — 24.44% of the total, almost level with gold and bigger than .US30Cash or EURJPY on their own. Tempting.

But the same market also has the lowest win rate of the five (32.49%) and the largest standalone drawdown (−131.21). That's the honest tension: a market can be a big profit contributor and still be the roughest ride in the book. So the question was never "can BTCUSD make money?" It's whether it behaves reliably under realistic execution, and whether it improves the portfolio once costs, spreads and crypto-specific risks are priced in.

At the portfolio level the five-market combination reaches a profit factor of 1.63 with a realised max drawdown of −158.71. That makes BTCUSD an interesting diversification candidate — emphasis on candidate, not conclusion.

Next step: validation, then a verdict

The focus now is careful out-of-sample validation of the Premium Fibonacci H4 direction — does its behaviour hold up outside the development sample, under realistic spreads and execution? Only after that, and a proper look at how it interacts with the rest of the book, will I decide whether BTCUSD earns its place beside XAUUSD, .US30Cash, BRENT and EURJPY.

That's the whole method in one line: a market doesn't get added because it looks good in a backtest — it gets added because it survives the validation the backtest can't do on its own.

Related reading

- Correct Builder Settings in SQ: Why Fixed SL, TP and Trailing Stops Must Be Normalized Per Market

- QuantMonitor Live Portfolio — Monthly Performance Update

- Benchmarking My Multi-Market Portfolio Against Darwinex INDX

- Base-market strategies: BRENT · EURJPY · Gold · Dow Jones

Your move: put a market through the same test

Reading about validation is one thing — running your own is where it compounds. So: pick a market you're curious about, build a few honest strategies, and see whether it survives real costs the way BTCUSD is being made to. You don't need my portfolio to start — just the next step.

Start free. Open a free QuantMonitor account, pull the free strategies and research, and see how evidence-first building works.

Tool up. The MetaTrader ToolBox cuts the StrategyQuant-to-MetaTrader grind — rename a whole databank in one click, deploy EAs to MT4/5, batch your backtests — so your time goes into strategies, not busywork.

Go all in. Premium is the full kit I open every week, and it's actively developed: templates (Fibonacci included), 9 workflows, StrategyQuant PRO, the Deployer toolbox and the video course — growing as I build, not a finished box.

Your next market is one disciplined backtest away. Take the step.

Research disclaimer: all portfolio figures above are based on historical backtest data and begin from zero cumulative equity, including recorded profit, swap and commission values. Historical performance is not a guarantee of future results — read the BTCUSD numbers as a portfolio research and validation view. Source of broker instrument availability: RoboForex BTCUSD contract specifications. Portfolio statistics are calculated from the combined QuantMonitor backtest databases for BTCUSD, BRENT, EURJPY, XAUUSD and .US30Cash.